Algorithm and Portfolio Stats: 04/22/2024 - 04/26/2024

It’s our first week of the new month with our algorithm - and it’s not good start. We’re down 24 bps, assuming equal allocations into all positions (17.9% allocation per position, based on average tickers traded per day). This isn’t good, but it’s within expectations for our low-mid 2’s Sharpe ratio projection.

The algorithm is still up overall, though obviously less compared to its cumulative gain as of the beginning of this week.

We’re going to continue as-is with the algorithm, as this level of performance in a single week isn’t a red flag performance-wise. If it continues under-performing, we’ll replace it with something different.

Speaking of, I’d like to discuss our “Experimental” algorithm. This one isn’t available to users - it’s exclusive to the HK team for private testing right now. Our public system takes a firm “Quality over quantity” approach, leading to only recommending a few trades each day. Our experimental system shifts the balance a bit, increasing the total quantity recommended each day (an average of 36.7 tickers traded per day, versus 5.6 on our public system). So far, our experimental system’s cumulative performance is slightly negative.

We’re going to continue running it, albeit with some reworks. We’re also looking to move a second experimental system into private testing this week. For this system, we’re dipping our toes back into machine learning, with random forest estimation. We feel that in this case, the existing trading technique will serve as effective feature engineering for an ML system, leading to superior performance.

We made 59 trades this week (43 long and 16 short) on 27 unique tickers. Let’s check them out.

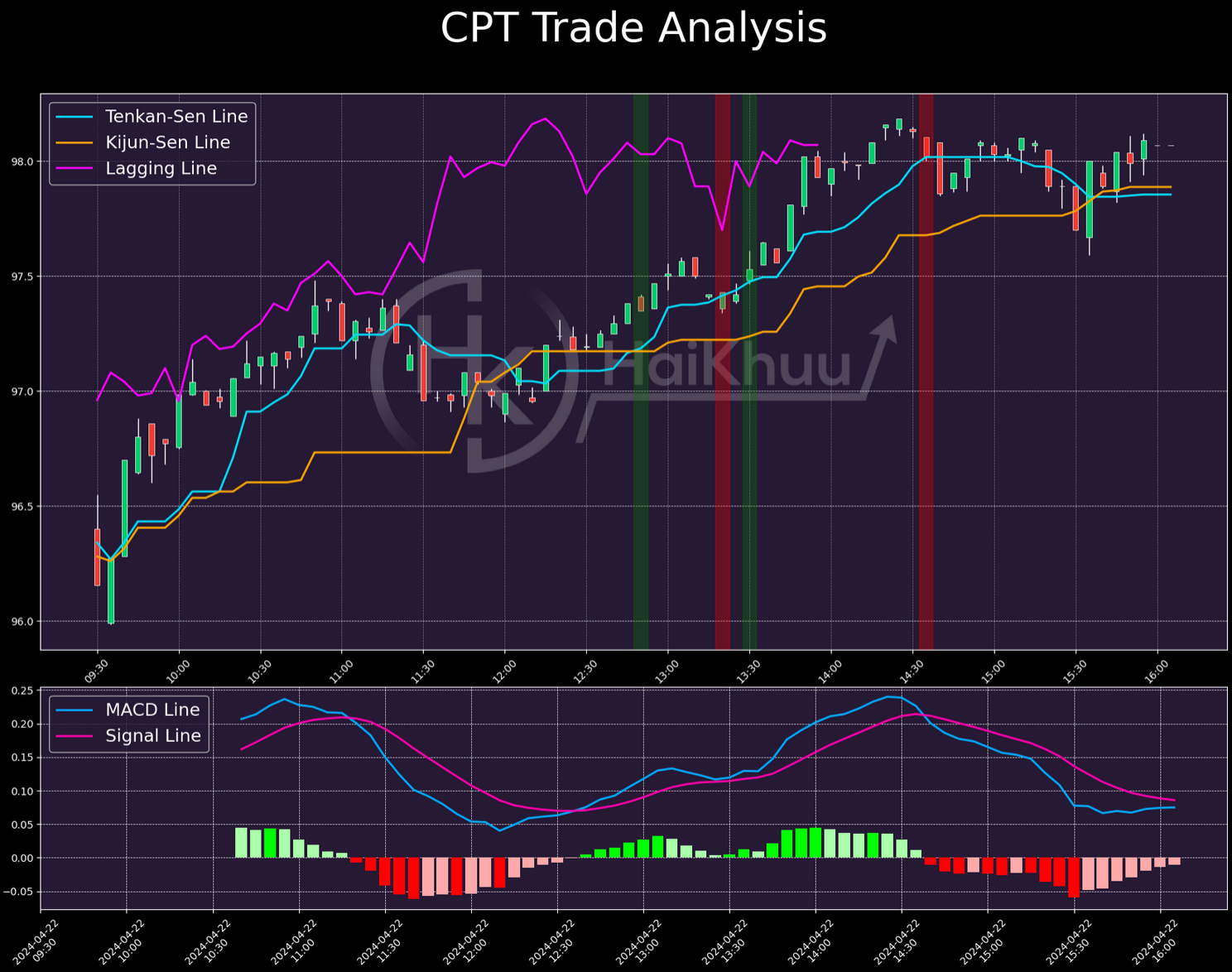

Our biggest winner of the week was a long trade on CPT, made on Monday. We made 0.54% across 2 entries. The only thing I think is questionable about this trade is our re-entry. The MACD differential is only slightly positive when we take that re-entry, though it does increase a good deal afterwards. The bullish momentum is pretty solid going into the re-entry, however, along with both TK-lines slowly sloping upwards, which helps mitigate this red flag.

Our biggest loser of the week was a long on PHM, taken on Tuesday. We lost 0.76% here, with just one entry. I’m gonna say pretty strongly that I wouldn’t have taken this one, and I think most of our traders would agree with me on that. The main thing driving this cross is a highly erratic opening stretch, combined with an equally erratic pre-market run. The bullish momentum behind that opening stretch had visibly died down by the time we entered, with the stock slowly approaching the level it dropped from during pre-market. While all of our signs are technically present (green MACD, lagging line in place, TK-Cross with price action above the Tenkan-Sen), this is a clear fake-out.

I don’t like seeing losing trades from our system, but at least there are plenty of red flags to a user, making this one pretty avoidable.

The last trade I want to highlight is this long position on O. There were no re-entries, here, and we made 0.41% on it. Even though this trade isn’t our biggest winner, I want to give it the spotlight because it’s just so clean. The MACD differential is increasing at an almost constant rate by the time we enter, we have roughly 7 straight candles of bullish momentum, with the Tenkan-Sen steadily sloping upwards plus very little erratic movement or chop previously that day. This is a rare trade with virtually no red flags to it. This is really the gold standard, not necessarily on the amount of profit, but consistency and great entry conditions. If you were watching our system on Monday, and checked out this notification, there was really very little reason not to take this one.

Now then, let’s examine our portfolio.

This week, we tried a defensive strategy with our portfolio - doing equal weighting of each ticker, as opposed to the market cap weighting we normally use. This was meant to lower our exposure to tech, in order to create a lower-beta portfolio. We did achieve our goal here - as this week, we were only over-exposed to highly defensive sectors: Consumer Staples, Energies, Financials, Healthcare, and Utilities.

While equal-weighting can successfully create a more defensive portfolio, upon re-examining, we don’t think it’s our best strategy at this time. Given SPY’s usage of market cap weights, if we want to compete with it directly, it doesn’t make sense to use a completely different strategy. Additionally, considering backtests going back as far as 1 year, market-weighting consistently out-performs equal-weighted portfolios. The biggest companies become big for a reason, and we want to take advantage of that.

This decision comes from Vlad - our head investment analyst. At this time, we feel there isn’t enough market uncertainty to justify this defensive strategy.

We finished under SPY this week (1.45% versus 2.10% returns), but given our return to market cap-weighting, we’re expecting to improve performance after this.

The results of this change are immediately visible. We’re back to tech being a plurality of our allocations, as well as a >1 market beta, plus over-exposure to the tech sector, relative to SPY.

As always, our portfolio for this week is listed below. For brevity, all tickers with allocations below 0.5% are excluded.

That’s all I have for you tonight. Thank you for reading - and happy trading!