Algorithm Performance: 09/26/2022

Performance Rankings

Experimental Sector Neutral: -0.05%

Sector Neutral: -0.07%

Market Neutral: -0.19%

Experimental Market Neutral: -0.23%

Long Term Portfolio: -0.46%

The Market: -0.57%

Base Algorithm: -0.71%

What Happened And Why?

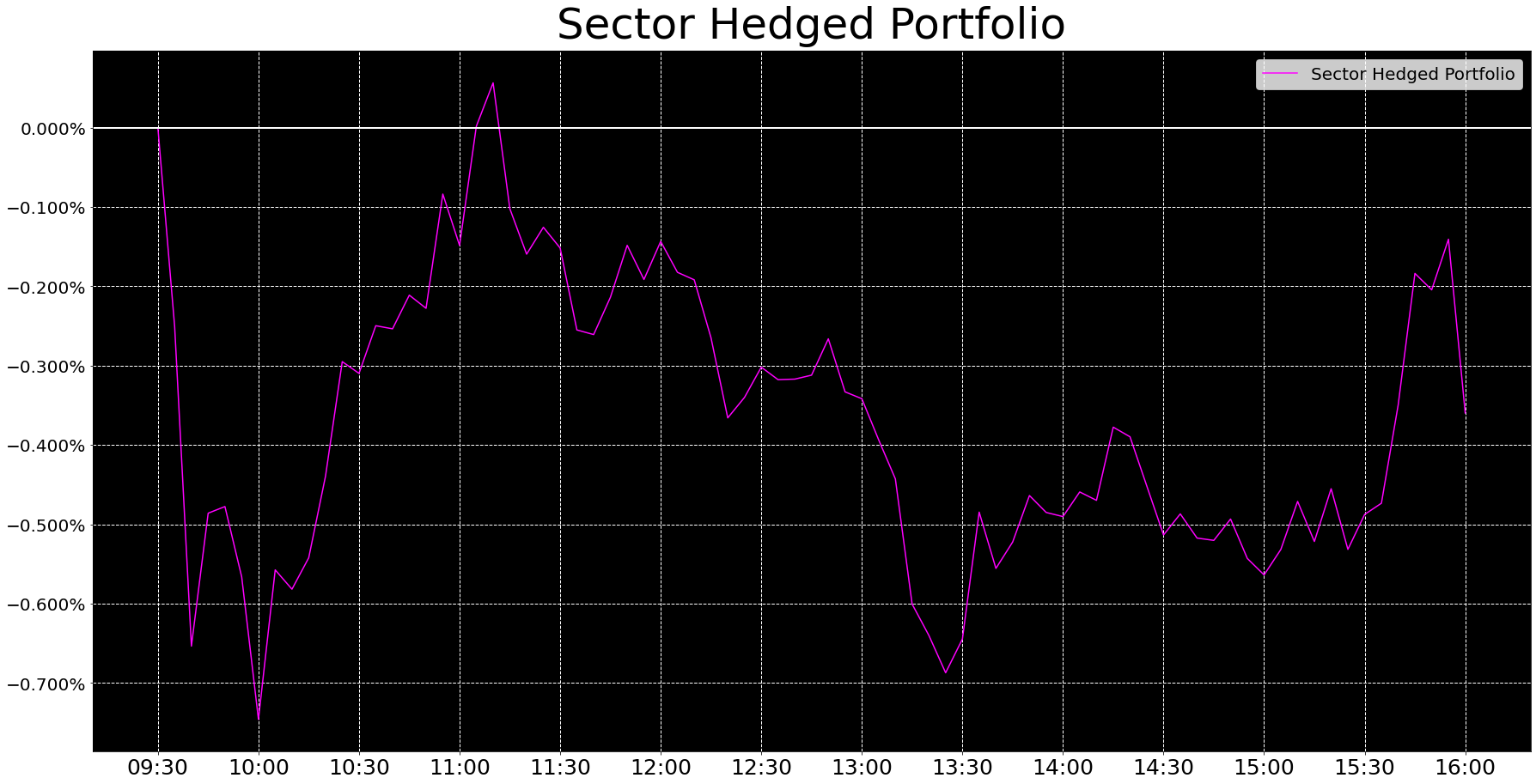

As expected, our technicals underperformed today. Since we saw this coming, we didn’t use them and did a modified sector hedge on our whole portfolio - that’s the one I’d like to dive into today.

At the beginning of the trading day, our hedged portfolio steeply dropped in value. While it came back later in the day, and our hedging was ultimately a net positive, I want to examine why that happened. And to do so, we have to contend with our margin restrictions.

Without accounting for cross-betas, changing the beta of your portfolio is easy. Just pick the ones you want to reduce to zero and short the corresponding sector ETF’s. Even if we do account for cross-betas between sectors, we should be able to completely reduce those betas by a similar set of trades. This set of trades can be determined with some linear algebra.

The trouble is that this solution is theoretical, because it doesn’t care what your beta limits are. To completely remove the betas of our portfolio, we’d need about 400% margin. As you might have guessed, this is way more than we’re willing to take on. Instead, we have to choose an amount of margin that we’re okay with, and prioritize which sectors are most important for us to hedge. The solution we came up with mostly reduced our betas, but slightly increased them in the energies and utilities sectors.

As you can see, these were the worst sectors be extra exposed to today. If we’d been able to perfectly reduce our exposures, today would have been a slam dunk. Even though our hedges ended up helping us, I’d feel much better if they’d been less volatile intra-day.

What Comes Next?

To reduce the likelihood of this happening again, plan A is to get a better hedge. We can give our optimizer more trade-ables to accomplish this without breaking our margin limits. The trouble is that, in order to do this, we’re either finding a list of things we don’t care about our exposures to, or giving the optimizer more goals it has to hit. I’m optimistic about this option, and think there’s a solid chance it works out.

Plan B is to ignore or de-emphasize cross-betas. We’ve done this with our sector-neutral algorithms to streamline backtesting, and it’s largely worked out for us. This isn’t an unattractive option by any means, but it would be great if we could do better.

Tomorrow’s Outlook

The full algorithm reports will be published tomorrow morning, once Allen has had a chance to vet its recommendations. In the meantime, here are our tentative exposures for the trading day tomorrow:

That’s all for tonight. Congrats to everyone who made money today. Let’s hope to see some more green tomorrow.

-Asher