Weekly Algorithm Review: 02/18/2023 to 02/24/2023

Algorithm Performance This Week

Market Neutral: +0.05%

Sector Neutral: -0.31%

Variable Market Neutral: -0.6%

Variable Sector Neutral: -0.65%

Long Term Portfolio: -1.1%

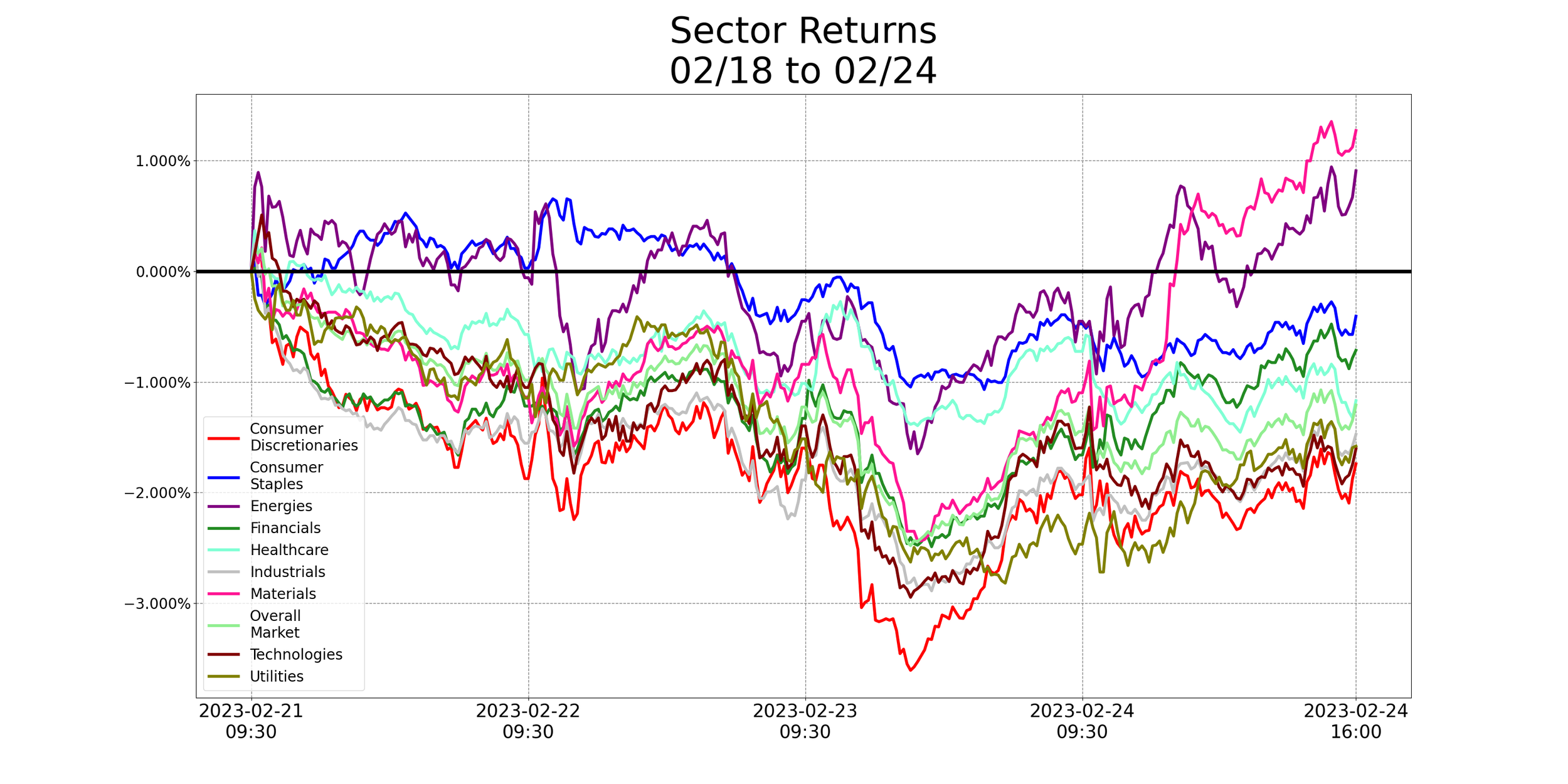

Overall Market: -1.21%

Base Algorithm: -1.3%

I’d like to start by thanking you all for your patience. As many of you know, we had a pretty substantial data loss issue on February 11th. We finished recovering everything last weekend - our algorithms were offline for about a week during that time. We’ve begun using a more rigorous backup system, which should prevent similar incidents in the future.

As for this week - results are slightly negative. The main way we evaluate the algorithm’s success is comparing the base system to the long term portfolio, and this week it under-performed by about 0.2%. While this is bad, I’m not considering it a red flag, as their performance is usually much further apart than that. This week, the algorithm’s performance was about neutral.

I want to note that all of our hedgers outperformed both the market and our long term portfolio, but given how bearish the market was this week, that’s mostly to be expected.

What’s In The Pipeline?

My main project right now is an integrated technical screener for our community. I’d like to be able to take in a watch list (current the entire S&P 500, but could also be community-determined), and a list of technical signals users are interested in, and send automated alerts whenever we see a buy or sell signal during the trading day.

For now, this is a standalone program, but at a later time I intend to integrate it with the intraday algorithm alerts we’ve been using. Currently, the algorithm uses the same protocol for every ticker to determine its target buy and sell prices. I can’t go into much detail here, but these target prices are only loosely based on technical signals. They take more influence from the ticker’s average performance on other days the algorithm has held it.

Once the screener is up and running, it’ll open the door for us to use more complicated entry and exit signals during the trading day. How much could we improve performance if, instead of having a fixed entry and exit price before the day starts, we could determine which technical signals had the best historic intraday performance for each ticker, and sent out buy/sell signals based on them?

Keep an eye on the HK server - I’m hoping to debut a basic screener this week.

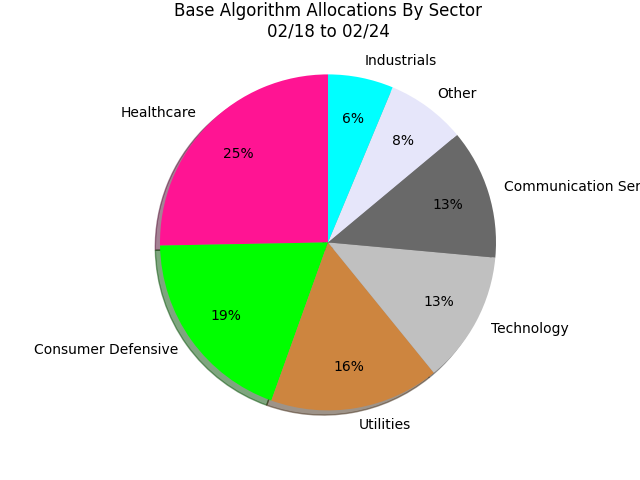

Misc. Data For The Week