Weekly Algorithm Review: 07/01/2023 to 07/07/2023

Performance Rankings

Overall Market: +0.5%

Long Term Portfolio: -0.07%

Base Algorithm: -0.18%

Variable Market Neutral: -0.54%

Variable Sector Neutral: -0.56%

Market Neutral: -1.04%

Sector Neutral: -1.34%

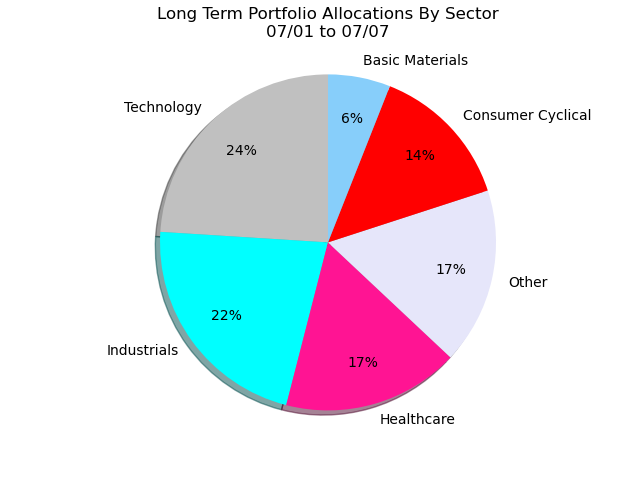

My hypothesis from last week has so far held true. We’ve gone from an outperformance of 4 bps from the algo to an underperformance of 11 bps. It seems the algorithm doesn’t want to diverge from this portfolio nearly as much as it did with our more defensive ones. Looking at our allocations by sector again, we see a similar pattern to last week.

It’s hard to point to a clear reason for this. One of the cons to machine learning systems is that they’re often very black-box. That is: it’s difficult to see exactly why it makes its decisions. I’d like to argue a reason I have in mind: a lack of major standout tickers. On our defensive portfolio, the algorithm was constantly putting 10%+ in NVDA, and almost as much into META. Here, the only stock that consistently breaks 4% is LRCX. This is unlikely to be the only reason for this change in performance, but it isn’t unrelated.

This raises an interesting question: how can we construct a portfolio that gives the algo the most ability to generate returns? So far, these results make me think that a larger portfolio would work in our favor. The algorithm doesn’t make strong choices very often (like NVDA, META, and to a lesser extent GOOGL), but of the ones we’ve seen, they’ve all worked out for us in the long run. I posit that, in future portfolios, we should try to increase quantity where we can - give the algorithm as many chances as possible to make those strong choices. It’s not a coincidence to me that, the moment we switch to a portfolio that yields more moderate allocations by the algorithm, we go from 150+ basis point wins, to being in the black 2 weeks in a row.

The timing of this wasn’t planned - but we’re actually switching to a new portfolio this week. This one is defensive, but not the same as our previous “defensive” portfolio. In the 2 weeks we’ve used this momentum-portfolio, the base algorithm underperformed it by 7 bps. Given the neglibility of this difference, and that we’re coming off of massive wins against our older, more defensive portfolio, I’m prepared to simply write this off and move on.

I want to note that, were we sticking with this portfolio for much longer, I would currently be doing more concrete research into how we could improve the algorithm’s performance here. Instead, my focus will remain on other projects. There isn’t much point into researching how we could improve performance on a portfolio that, in 24 hours time, we won’t be using anymore. My research time is simply better spent elsewhere.

What’s In The Pipeline?

In the interest of full disclosure: I had Covid this week, and wasn’t able to make as much progress on things as I would have liked.

The signal from last week is still being worked on. We’ve managed to expand the average length of its signals - a buy/sell has gone from lasting an average of 115 seconds to about 5 minutes under our current model. This model also reduces the average positions per ticker per day from around 60 to around 6.

We’ve found that to maximize performance in backtests, we don’t want to run this on every ticker each day. Instead, we want to select only tickers well-suited to this indicator. Interestingly, we find we can preserve the strength of our results using as few as 10 tickers each day. This means we’re only looking at 60 buy (or short) signals per day - a much more reasonable number than what we were looking at earlier!

At this point, I would definitely expect updates on this signal in the future.

Misc. Data For The Week