Weekly Algorithm Review: 07/29/2023 to 08/04/2023

Performance Rankings

Sector Neutral: +0.59%

Variable Sector Neutral: -0.36%

Market Neutral: -1.15%

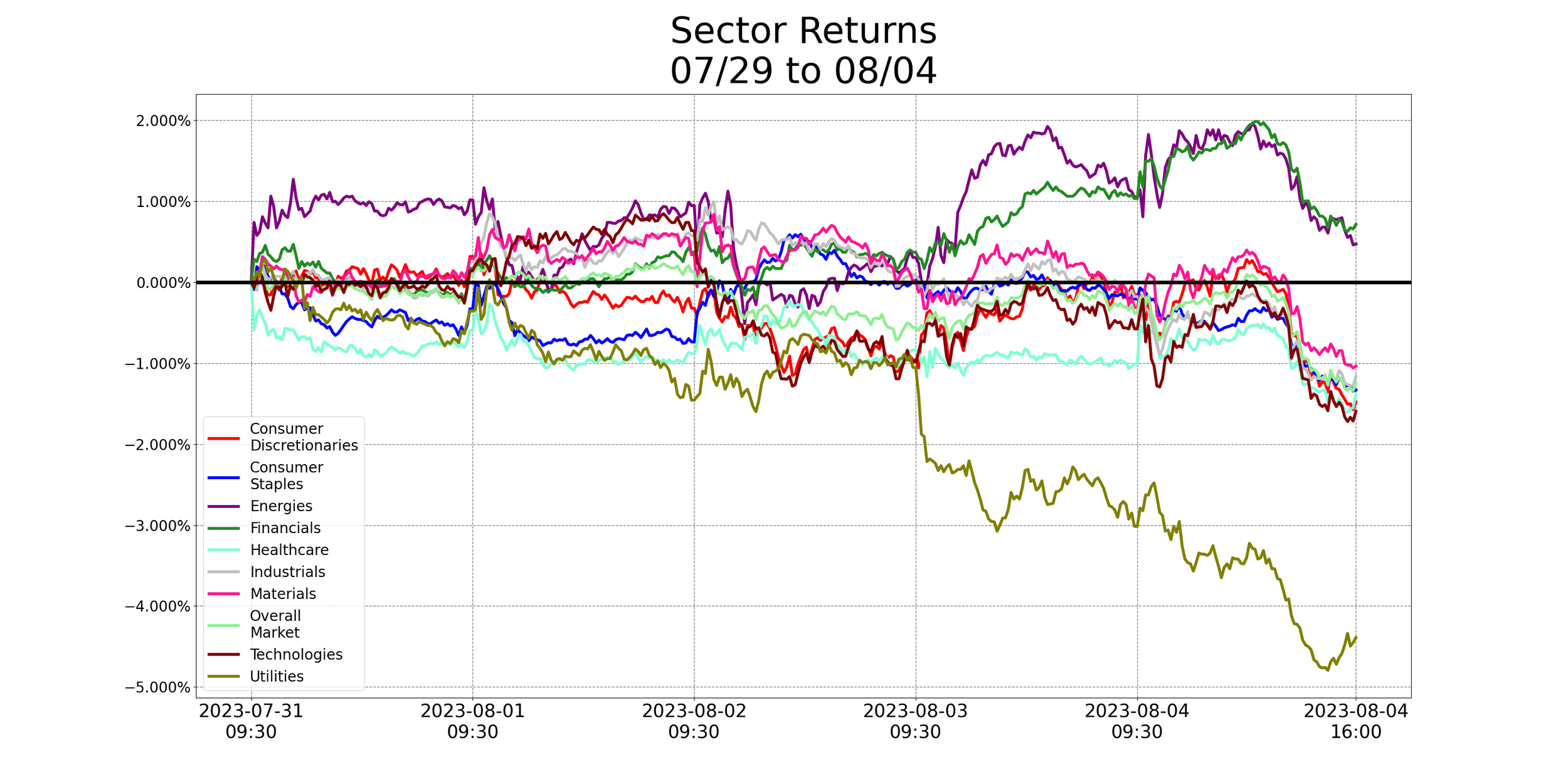

Overall Market: -1.25%

Variable Market Neutral: -1.69%

Long Term Portfolio: -1.85%

Base Algorithm: -1.95%

This was a tough week for us. Our portfolio under-performed the market by 60 bps, and the algorithm by a further 10. At this time, we still feel good about our defensive long term portfolio - especially after the market’s performance on Friday coupled with the news of fewer jobs and more inflation.

The algorithm is, in total, green over the portfolio over the last 2 weeks - albeit slightly. Every week the algorithm under-performs the portfolio is, of course, undesirable - but 1 isn’t a red flag in and of itself. Our current goal for the algorithm is the following: if we take the returns of the algorithm, and subtract the returns of the portfolio, we should achieve a Sharpe of 3.0 or greater. I wouldn’t say we’ve definitively reached that yet, but when we do development work on the algorithm, that’s the benchmark we’re striving for.

In order to achieve it, the algorithm doesn’t have to out-perform the portfolio every single week, but it needs to win more often than it loses, and its wins need to be bigger than its losses. So far this quarter, the algorithm has been green over the portfolio in 6 weeks, and red in 3 of them. Its average weekly loss is roughly 9 bps, while its average weekly win is around 60 bps. So far, our numbers are looking good. The algorithm usually wins, and wins more than it loses. For this reason, we don’t look at individual red weeks as major problems. It’s only if they start coming more consistently that we get concerned. Currently, this level of performance is within our expectations.

What’s In The Pipeline?

Vlad and I are looking into changing up our long-term portfolio. We want to maintain our defensive, market-bearish thesis for the time being, but we’re interested in broader portfolios. Based on the algorithm’s performance with previous portfolios, I have a hypothesis that it does better when given a more diverse range of options. A change to our portfolio will of course be contingent on Vlad being confident in it for the long term, and the algorithm indeed performing better with it in backtests.

That aside, my focus remains on continued experimentation with the main algorithm, as well as research into new intraday signals. I can’t give a clear picture of when an update to the main or intraday algorithms are coming, but we’re constantly working towards it.

Additionally, some work is ongoing with the news bot. We’ve made a few modifications to it, which have improved its consistency over the last week. But we think it can be better. Expect further changes to further reduce unnecessary news alerts.

Misc. Data For The Week