Weekly Algorithm Review: 04/08/2023 to 04/14/2023

Overall Market: +0.63%

Long Term Portfolio: +0.57%

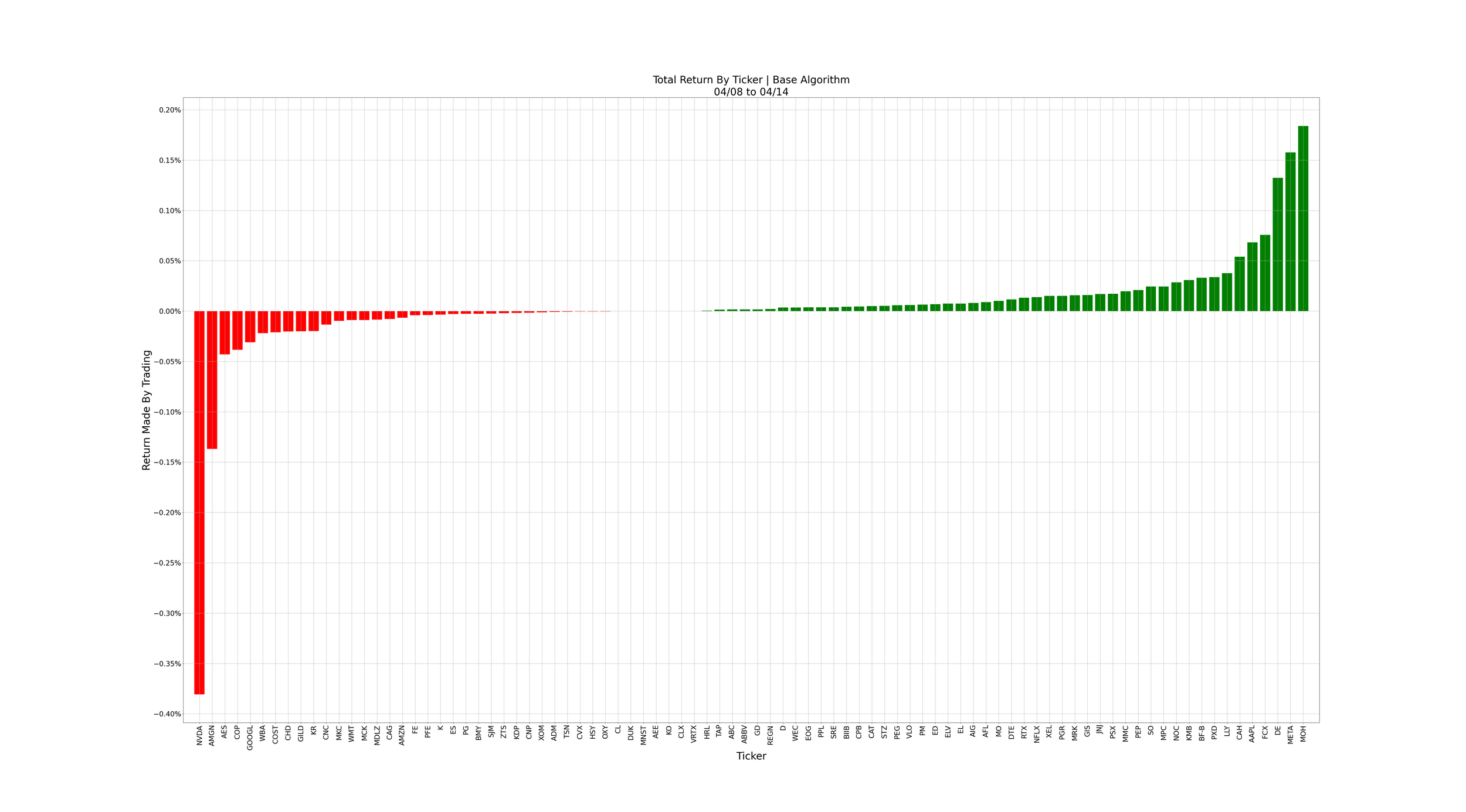

Base Algorithm: +0.34%

Variable Sector Neutral: +0.29%

Variable Market Neutral: +0.19%

Sector Neutral: +0.02%

Market Neutral: -0.11%

With a small loss from technicals (23 bps), and a smaller loss from fundamental analysis (6 bps), we underperformed the market this week.

The culprit is obvious - the algorithm’s heavy allocations into NVDA. It bet disproportionately heavy on tech, during a week where tech was one of the weakest sectors. Had we held no NVDA this week, the base algorithm would have beaten the long term portfolio handily. That said, I’m not currently identifying this behavior as problematic.

Despite a rough week, NVDA has worked out great for us in the long run. At this point, it’s unlikely for the algorithm to lose anywhere close to what it’s made trading it. Rather than retreading discussions of the algorithm’s ability to predict macro trends, I’d like to discuss something new: what would it take for us to want to change the algorithm? When would we step in and say “It’s taking too many losses on X stock, and has to be stopped at the software level”?

It’s a simple question with a complicated answer. The short version is: multiple consecutive weeks of large losses from the same offenders, or multiple consecutive months of under-performance. NVDA was one of our biggest holdings this week, and the biggest source of losses by a large margin. If we see that consistently, without the algorithm reducing its position, that would be a big warning sign for me.

Based on backtests and live results, we estimate our trading algorithm to have a Sharpe Ratio in the mid-2’s or higher. That requires heavy generalizing, as it depends on factors like the long term portfolio, the market’s performance overall, and of course the variance you get from trading with technical signals. A Sharpe in that range means that, while we expect some red weeks, red months should be a rarity. Should this not match what we’re actually seeing, it might be time to re-evaluate the algorithm.

I want to take a second to say that, during development of the algorithm, we considered implementing measures to force it to take more even diverse allocations. We didn’t roll these out because, in backtests, they reduced our Sharpe. Diversification is something we incorporate into every version of the algorithm we test; we roll out the version with the strongest backtest performance. The only reason the algorithm is allowed to take large stakes in individual stocks is that, of the models we’ve tested, this one leads to the best results.

I also want to clarify that, should this happen, it wouldn’t mean the algorithm has been a failure. In fact, this is to be expected eventually. Trading algorithms come in and out of effectiveness over time. As the markets evolve, it’s important to let your strategies evolve with them. If you used carrier pigeons to arbitrage in the 1800’s, you would have been fabulously successful. Now, only the most high-frequency of high-frequency trading companies can consistently pull that off. Richard Donchian came up with his titular “Donchian Channels” in the 1930’s, Goichi Hosoda his “Ichimoku Clouds” in the 1960’s. Now they’re both just components in more advanced modern trading models.

The market evolves quickly. If you don’t evolve with it, it will leave you behind. The job of a Quant Trader isn’t just coming up with strategies, it’s watching them in action and determining when it’s time to evolve them.

This is all to say that: should the algorithm fail to perform at our target levels, we will withdraw it and return to the drawing board. At this time, it is performing safely within our expectations of it. Normally, I would be experimenting with the algorithm every day, to determine what could be improved and pitch new ways to give it an edge. These days, my priorities are mostly in shorter term projects to expand HaiKhuu. When we do finally launch the mutual fund, I intend to return to my ways of having the algorithm as my sole project.

Misc. Data For The Week